"Must haves" for engineering software investments

August 04, 2015

It seems that in recent years, investing in technology companies has again become detached from the fundamentals. We're back to the casino game of "ge...

It seems that in recent years, investing in technology companies has again become detached from the fundamentals. We’re back to the casino game of “get in, watch carefully and try to get out again at a point where the price is higher than you paid.” It’s hard to see what this sort of hit-and-run investing does for the economy; for one thing, it drives a damaging misallocation of capital. But one area of technology investment still looks good on the basis of fundamentals and supports the productive areas of the economy – engineering software.

Before we look at why the engineering software market offers sound investment opportunities, let’s define its scope and size. It covers the wide range of applications used by engineers and designers in manufacturing, architecture, construction, utilities, and other sectors. So that’s CAD, CAM, CAE, PLM, etc. in manufacturing; BIM and related applications in architecture, engineering, and construction (AEC); geographic information systems; and even applications like visual effects (VFX) that are increasingly used to visualize designs. With the trend toward smart devices, the scope now needs to include the tools used for embedded software development. Taking this scope, the core market was around $25 billion in 2014.

What about the fundamentals? Figure 1 tracks worldwide growth. Since a fall in 2009 following the 2008 crash, the market has returned to growth despite the on-going economic problems. Figure 2 shows the variation by region. Figure 3 shows the distribution of the market by the top 10 countries.

|

|

|

|

|

|

So from an investment point of view, engineering software has shown great resilience. One reason for this is that there are benefits irrespective of the user organization’s circumstances. They range from reduced costs and streamlined product development processes to better designs and the ability handle more complex products, up to integrated product life cycle management.

A second reason for continued growth is that engineering software is being adopted in ever-increasing areas of activity. In manufacturing industries, from origins in the product design and development phases of a product’s life, engineering software is being exploited right across the product life cycle, supporting new ways to provide after-sale maintenance and support and closing the loop between innovation and field use.

With the increased use of smart networks for managing production and even in the design and development phases, it’s being supporting new collaborative approaches and processes. In the architecture, engineering, and construction (AEC) industries, the growing use of building information management (BIM) to integrate not only design but also facility operation across its lifetime is generating numerous application and integration technology opportunities.

Then there’s the question of exit. The engineering software market’s nature, structure, and dynamism mean that for the right businesses, there are excellent exit opportunities. The major players now primarily seek a competitive advantage by breadth of integrated solution portfolio rather than by focused product capabilities; the sheer range and number of the applications required to achieve this makes it impossible for them to develop everything in-house. Consequently, recent market history has featured a string of strategic technology acquisitions by the dominant companies.

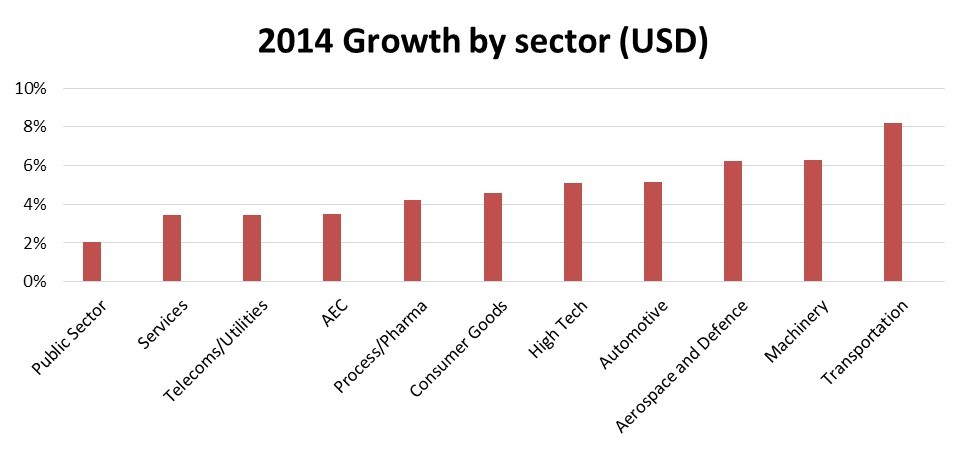

The trick, of course, is to identify the right technologies in the right sectors. The engineering software market is very complex, spanning almost all parts of the world and covering a huge number of industries and products for a wide range of activities. Like most markets, it also has its mature areas, where growth is modest but steady and entry is difficult. Furthermore, many customers have made substantial investments in their engineering software infrastructure, with well-established incumbent product sets supporting their product development workflows. Looking at various perspectives can be very helpful. For example, the chart in Figure 4 shows growth in 2014 by high-level industry sector.

|

|

The combination of market complexity and maturity means that evaluating investment opportunities is a multi-dimensional task, requiring many perspectives. Nevertheless, if done carefully, the investment outcomes in the engineering software market can be very positive. Investing in the Engineering Software Market was the subject of a recent Cambashi webcast.

Tony Christian brings to Cambashi wide ranging experience in engineering, manufacturing, energy and IT. Previously, he was a director of the UK Consulting and Systems Integration Division of Computer Sciences Corporation (CSC), leading a consulting and systems practice for manufacturing industries, and then Services and Technology Director at AVEVA Group plc where he was responsible for all product development and the company’s worldwide consulting and managed services business. Tony holds a BSc degree in Mechanical Engineering and an MSc degree in Engineering Acoustics, Noise, and Vibration, from the University of Nottingham.